Buy Now, Pay Later Lifts AOV 20-40%. Here's How to Add It Without Killing Margin

Buy Now, Pay Later can lift AOV 15-40% and conversion 20-30%. See the fee math, the right provider for your store, and how to add BNPL without killing margin.

A shopper fills their cart with $180 of your product, gets to checkout, sees the number, and quietly closes the tab. Nothing was wrong with your site, your price, or your product. The total just felt like too much to pay all at once on a Tuesday. Now imagine that same checkout showing "or 4 payments of $45" right under the price. That one line is the difference between a lost cart and a completed order, and it is why Buy Now, Pay Later stopped being a big-brand feature and became table stakes for stores doing $500K to $10M.

BNPL is not new. What changed is the scale. Global BNPL spending is on track to clear $565 billion in ecommerce this year, roughly 96 million Americans will use it in 2026, and it now accounts for 5 to 6% of all online payment volume worldwide. Your customers already pay this way everywhere else they shop. The only question is whether your checkout lets them.

What BNPL actually is in 2026 (and what it costs you)

Strip away the branding and there are really two products hiding under the "Buy Now, Pay Later" label, and they behave very differently.

The first is Pay in 4: the customer splits the purchase into four interest-free payments over six weeks, first installment at checkout. This is what Klarna, Afterpay, and Shop Pay Installments push hardest, and it is the one that moves the needle for most stores. The second is longer financing, three, six, or twelve months, usually with interest paid by the customer. Affirm built its business here. Financing matters if you sell mattresses, bikes, or anything north of $500. For most stores under that price point, Pay in 4 is the whole game.

Here is the part that surprises owners: you get paid in full, upfront. The BNPL provider fronts the customer the money, pays you within a couple of days, and takes on the collection risk and the fraud risk. If the customer never finishes their four payments, that is the provider's problem, not yours. You are not becoming a lender. You are renting theirs.

That service is not free. The provider takes a cut of every BNPL order, and it is meaningfully higher than a normal card fee:

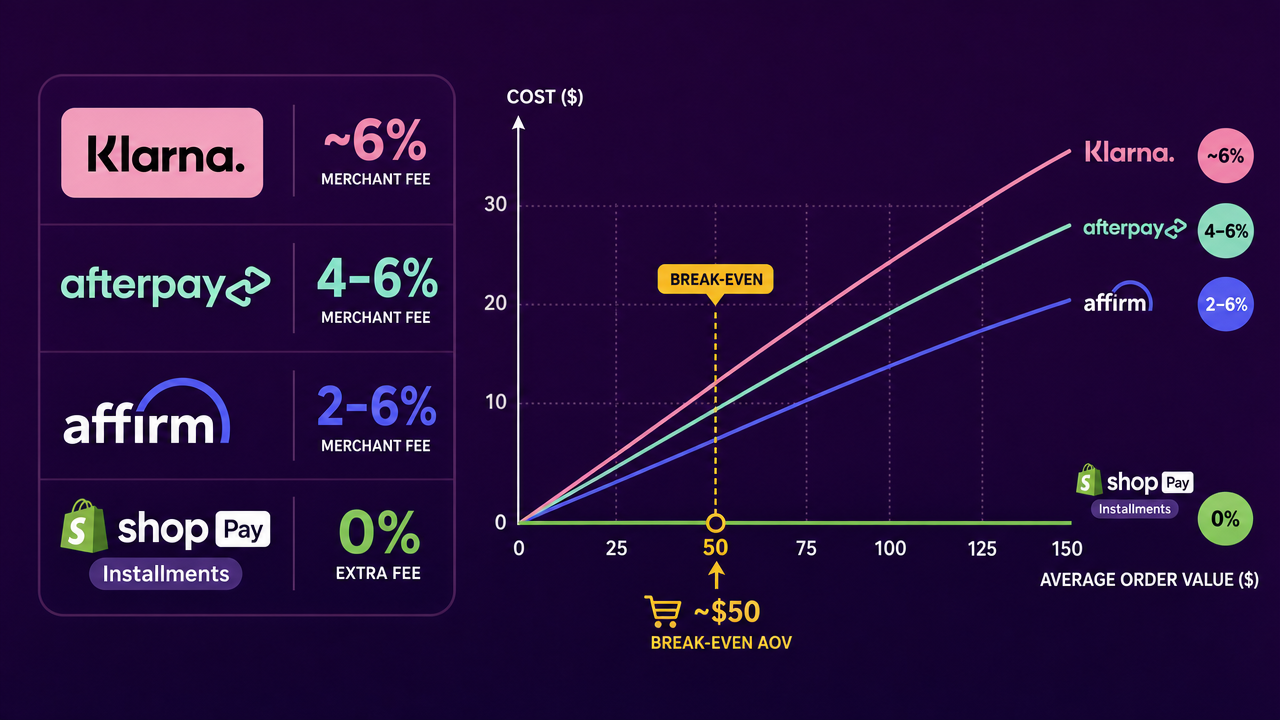

- Klarna: around 5.99% + $0.30 per transaction for most merchants, negotiable down toward 3.29% once you are past roughly $5M in annual volume

- Afterpay: 4 to 6% + $0.30, with the exact rate tied to your volume and category

- Affirm: 2 to 6% depending on the financing term you offer

- Shop Pay Installments: no extra merchant fee beyond your standard Shopify Payments rate if you are a US Shopify store already on Shopify Payments, which makes it the cheapest on-ramp by a wide margin

Compare that to the 2.3 to 2.9% you already pay on a normal card and BNPL looks expensive. It is. The entire decision comes down to whether the lift in order value and conversion covers that extra spread. Usually it does, but not always, and the math is more specific than the vendors want you to think.

The AOV lift is real. Read the fine print anyway.

Every BNPL provider will wave a giant number at you. The honest range, across independent studies rather than vendor case studies, is an average order value lift of 15 to 40% and a conversion rate lift of 20 to 30%, with cart abandonment dropping by as much as 35%.

Those are strong numbers. But the outliers get quoted as if they were typical, and that is where owners get burned. Affirm likes to cite an 87% AOV increase. Afterpay quotes 20 to 40%, concentrated in fashion and beauty. PayPal's own data on small and midsize merchants is more grounded: about a 20% higher AOV on Pay Later orders versus standard ones. When a real deployment gets measured end to end, the numbers get more sober still. A 2026 Klarna rollout across five markets produced a 21.5% conversion-rate improvement and a 25.3% jump in revenue per visitor, but only a 3.3% AOV lift. The conversion gain did the heavy lifting, not the basket size.

The takeaway is not "BNPL doesn't work." It clearly does. The takeaway is to expect a solid double-digit conversion improvement and a modest-to-strong AOV bump, then let your own data confirm it, rather than budgeting around a cherry-picked 87%.

The break-even math nobody runs before switching it on

This is the single calculation that decides whether BNPL makes you money or quietly bleeds it, and almost no one runs it before flipping the switch.

Take your average order value. Multiply the fee difference between BNPL and your normal card rate (call it roughly 3.5 percentage points for a Pay in 4 provider). That is what each BNPL order costs you on top of a card order. Then ask: does the extra conversion and basket size cover that?

Work a real example. Say your AOV is $40 and Klarna charges you about 6%. That is $2.40 per order in fees, versus roughly $1 on a card. You are paying an extra $1.40 to process that sale. On a $40 order with a thin retail margin, that $1.40 can eat a real slice of your profit, and if BNPL only nudges your basket from $40 to $42, you are underwater. Now run the same math on a $180 order. The extra fee is around $6, but if BNPL lifts that basket 20% to $216 and converts a shopper who would otherwise have bounced, you are comfortably ahead.

The rule of thumb that falls out of this:

- BNPL earns its fee when your AOV is above roughly $50, and it shines above $100

- Below $30 AOV, be careful. The percentage fee plus the flat $0.30 can outrun the lift, especially on impulse-priced goods

- Thin-margin categories need a higher AOV floor to absorb the spread than high-margin ones do

If you are wrestling with margin pressure already, BNPL fees are one more line to defend, which is exactly the kind of trade-off we walked through in tariff-proof pricing. Add the fee to your pricing picture on purpose, do not let it surprise you at month-end.

Which provider actually fits your store

Provider choice is less about brand and more about where your customers and your platform already are.

If you are a US Shopify store, start with Shop Pay Installments. It rides on Shopify Payments, adds no extra fee beyond what you already pay, and turns on in a few clicks. There is almost no reason not to have it live. It is the closest thing to a free conversion bump in ecommerce right now.

If your customers skew younger and shop fashion, beauty, or accessories, add Afterpay or Klarna on top. Both have huge built-in app audiences that actively browse their marketplaces for stores that accept them, so you get a small discovery channel on top of the checkout option.

If you sell high-ticket, considered purchases (furniture, fitness equipment, electronics over $500), Affirm's longer financing is the one that unlocks the sale. Nobody splits a $2,000 sofa into four two-week payments. They want twelve months, and the customer, not you, carries the interest.

You do not need a separate merchant account for any of these. Klarna, Afterpay, and Affirm all ship plugins for Shopify, WooCommerce, and Magento that drop BNPL in as an extra option alongside your existing gateway. Setup is an afternoon, not a project.

Put the message on the product page, not just at checkout

Here is the mistake that quietly caps most BNPL results: stores bolt it on at the final checkout step and nowhere else. By then the shopper has already decided whether the price feels affordable. The decision to abandon happens earlier, on the product page, when they see the full number for the first time.

The stores getting the big conversion lifts show the installment breakdown everywhere the price appears:

- On the product page, directly under the price ("4 interest-free payments of $45")

- On the collection and category pages, so the per-payment number frames the product before the click

- In the cart drawer, right as hesitation peaks

That on-site messaging is where the measured 20%+ conversion gains actually come from. It reframes a $180 product as a $45 one in the shopper's head before sticker shock can do its damage. If your checkout is also slow or clunky, the BNPL message will not save it. Fix the friction that leaks revenue at checkout first, then let BNPL amplify a checkout that already works.

The trust and regulation reality you should not ignore

BNPL sits in a genuinely messy regulatory spot right now, and pretending otherwise is how brands end up with angry customers.

The consumer side is not all upside. In 2026, 47% of BNPL users reported missing at least one payment in the past year, up 6 points from the year before, and BNPL users carry meaningfully more credit card and personal loan debt than non-users. On the oversight side, the CFPB withdrew its 2024 rule that had extended credit-card-style protections to BNPL, which means fewer built-in dispute rights for your customers in the US for now. Meanwhile the UK's FCA begins formal BNPL oversight in July 2026, several US states are writing their own frameworks, and BNPL activity is increasingly reported to the credit bureaus.

What that means for you as a merchant is simple and worth doing right:

- Be transparent in your messaging. Show the real terms, not just the happy "4 payments" line. Customers who understand what they are signing up for churn and chargeback less.

- Let the provider own the lending relationship. You are offering a payment option, not financial advice. Keep your copy about convenience, not about "affordability" claims you are not licensed to make.

- Watch your returns flow. BNPL refunds route back through the provider, which can confuse customers expecting instant money back. A clear returns note prevents most of those support tickets.

Handled cleanly, none of this is a dealbreaker. It is just the difference between BNPL as a trust-builder and BNPL as a complaint generator.

What to do this week

You can have this live and measured inside of a week without a developer sprint:

- Pull your AOV and your gross margin. If your AOV is above $50, BNPL is very likely worth it. If it is under $30, run the break-even math above before you commit.

- Turn on the cheapest option first. US Shopify store? Enable Shop Pay Installments today, it costs you nothing extra. Everyone else, install the Pay in 4 provider whose audience matches your customers.

- Add on-site messaging to your product pages, not just checkout. This is where the conversion lift is won or lost.

- Pick one metric to watch for 30 days: conversion rate on BNPL-eligible traffic, or AOV on BNPL orders versus card orders. Let your own numbers, not the vendor's deck, tell you if it is working.

- Write one clear line of returns and terms copy so the trust side is covered from day one.

BNPL is not magic and it is not free, but for a store with the right price point it is one of the highest-leverage checkout changes you can make this quarter. It turns a number that scares people into one that feels easy, and it does it on the provider's balance sheet, not yours.

If you want a second set of eyes on whether BNPL pencils out for your specific margins, or on the checkout flow it is supposed to amplify, book a call. Bring your AOV, your margin, and your current cart abandonment rate, and we will tell you on the call whether BNPL is your next win or a distraction from a bigger leak.

Reviewed by Keston Leader under our editorial policy.